While purchasing the policy most of the times we ignore this condition and at time of claim we end up paying a portion of Hospital Bills even though we hold Health Insurance policy. Let us understand why you have to face this scenario?

What is Co-payment?

Co-payment in the Health Insurance is the fixed % have to pay by Policyholder at the time of claim in your Hospital Bills. This has to bear by your own pocket and rest of the Claim amount will be settled by Insurer.

Co-payment usually applies 20%, this may vary from policy to policy from 10% to 50% too.

Let see this in the example:

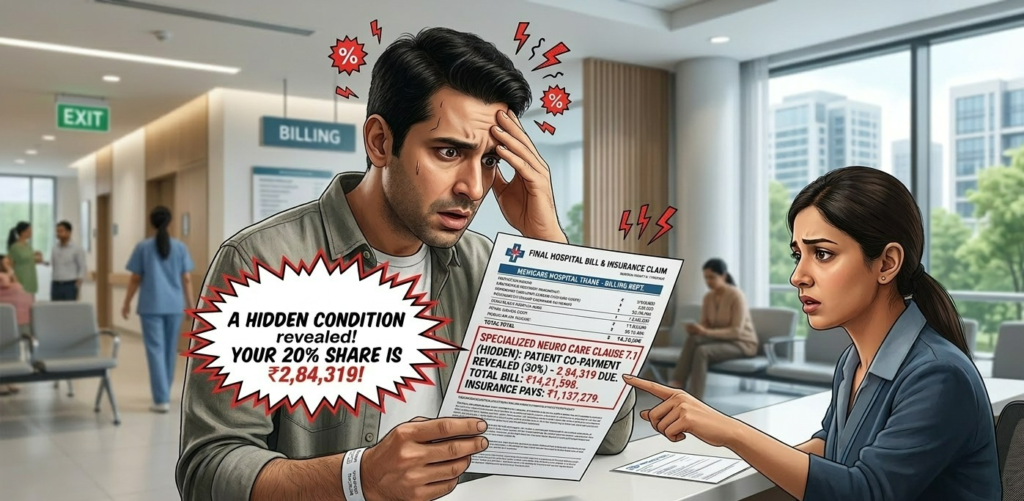

Imagine you have a health insurance policy with a 20% co-payment clause. If you are hospitalized and the final bill comes to ₹1,00,000, here is how the payment is split:

Item | Amount |

Total Hospital Bill | ₹1,00,000 |

Share (20% Co-pay) | ₹20,000 |

Insurance Company Pays | ₹80,000 |

Even though you have insurance, you still have to shell out ₹20,000. If the bill was ₹10,00,000, your share would jump to a massive ₹2,00,000.

Why Co-payment was introduced?

In order to decrease the premium and the client can fall in this trap without knowing to them. In this scenario client will think to buy finding cheap and lower premium and he will least ignore the term and condition.

When the policyholder buys the policy with copay, he will get 20% less of his total expense spend on Hospital bills.

Why You Should Avoid Co-pay When Buying a Policy

When you are comparing plans, a “Co-pay” policy will often have a lower premium (the yearly price you pay) than a “No Co-pay” policy. This is the bait. Sales agents might highlight the lower premium to make the deal look attractive, but here is why you should choose a policy without co-payment:

- Peace of Mind:With a “Zero Co-payment” policy, the insurer pays the entire admissible claim amount. You can focus on recovery rather than your bank balance.

- Long-term Savings:Saving a few thousand rupees on your annual premium isn’t worth the risk of paying lakhs during a claim. One single hospitalization can wipe out years of “premium savings.”

- Age Factors:Many policies for senior citizens have mandatory co-payments. If you are young and healthy, buy a “No Co-pay” plan now so you can keep that benefit as you get older.

Conclusion – So should we opt the Co-payment or not? Verdict is No “Big No”, simply it will be burden to you and will always be in a trap. Always ask with your Agent or Customer Care guy ahead about copayment is applicable or not in your policy. Generally, you should buy policies without a co-pay even if the premium is high Generally, you should buy policies without a co-pay even if the premium is high.

Amount paid by you at time of claim will be always higher than the premium you paid.