When you’re purchasing for health insurance, it’s easy to focus solely on the Sum Insured and the Premium. But the two most crucial sections of any policy—Since when you can start utilize your Sum Insured with this condition applicable are the Waiting Periods and the Exclusions.

Understanding these concepts is the key to preventing a claim rejection. This blog breaks down how they work, the different types of health insurance, and how “add-on riders” can sometimes waive these rules.

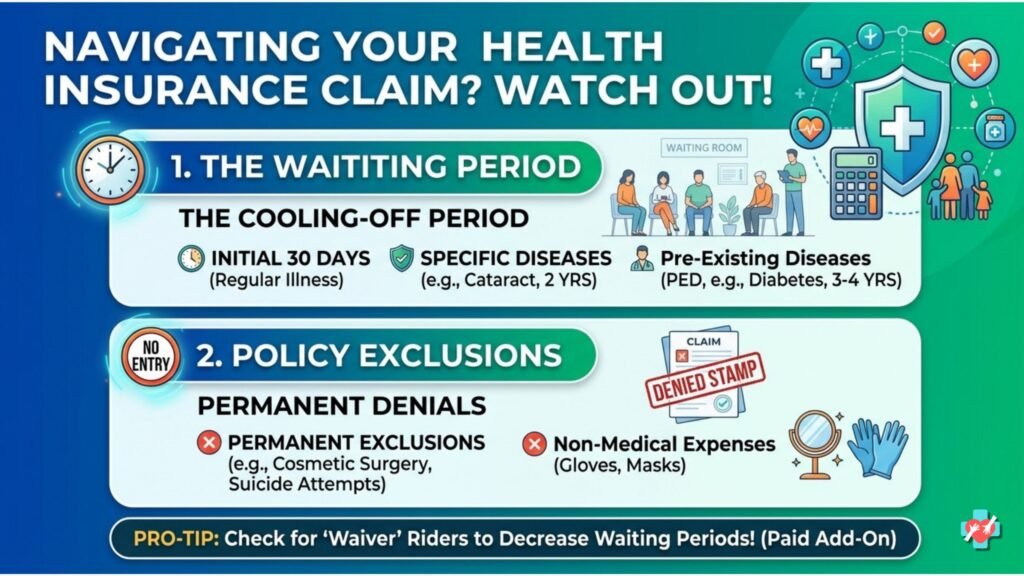

- Decoding Waiting Periods: The “Cooling-Off” Rule

A Waiting Period is a mandatory timeframe, starting from the policy’s effective date, during which you cannot make a claim for certain specific illnesses. If you fall ill during this window, you must pay the bills yourself, even though you have an active policy.

In the Indian market, waiting periods typically come in three types:

- Initial Waiting Period (30 Days)

This applies immediately after the policy starts. You cannot make a claim for any regular illness (like viral fever, dengue, or infection) within the first 30 days.

- The Exception: Claims resulting from an accident are covered from Day 1.

- Specific Illness Waiting Period (2 Years)

This applies to a listed set of “slow-growing” conditions that insurers believe could have been developing before you bought the policy. Even if you didn’t know you had them, a 2-year waiting period usually applies.

- Common Examples: Cataracts, Kidney stones, Hernia, Piles, Joint Replacements, and internal tumors.

- Pre-Existing Disease (PED) Waiting Period (3 Years)

A PED is any medical condition, injury, or ailment you had before purchasing the policy. The insurer will impose a waiting period (3 years) for any claim related to that specific illness.

- Example: If you declare Diabetes when buying the policy, a claim related to Diabetic retinopathy will be rejected during the 4-year waiting period.

- Decoding Exclusions: What Is Never Covered

While waiting periods are temporary, Exclusions are permanent. They are conditions, treatments, or situations that your health insurance policy will never pay for, under any circumstance.

- Permanent Exclusions

These are general and often include:

- Cosmetic or aesthetic surgeries (unless reconstructive due to accident).

- Obesity or weight-control treatment.

- Injuries due to adventure sports or participation in dangerous activities.

- Injuries resulting from illegal activity, suicide attempts, or substance abuse (alcohol/drugs).

- Alternative treatments like Naturopathy or experimental therapies (unless specifically specified as AYUSH cover).

- Non-Medical Exclusions (The “Consumables”)

These are specific items on a hospital bill that insurers refuse to pay.

- Common Items:Gloves, masks, gowns, nebulizer kits, hygiene items, and registration fees.

- Can I Get a Waiver or Buy These Off? (Yes, sometimes!)

Policyholders are often frustrated by these long waiting periods. Insurers have introduced specific solutions—for a price—that allow you to waive or reduce these periods.

- Waiting Period Reducer Riders

An add-on rider is an optional feature you purchase alongside your main policy. Some riders allow you to pay an extra premium to shrink your PED waiting period from 3 years down to 2 years or even 1 year.

- Pre-Existing Disease Waiver

This is a more powerful (and expensive) rider where you pay a significant extra premium to have specific pre-existing conditions covered from Day 1 (usually after a mandatory initial 30 or 90 days). This is very popular for senior citizens or individuals with critical but managed conditions (like stable hypertension).

- Specific Illness Waiver

You can sometimes find riders that waive the fixed 2-year waiting period for specific surgeries (like Cataract).

- Consumables Cover

A very useful rider that, for an extra fee, covers those typically excluded 60+ “non-medical” items (gloves, masks, etc.), which can add up to 10–15% of your total bill.

- Voluntary Deductibles / Copayment

This is the inverse strategy. By agreeing to pay a certain fixed amount (a “Deductible”) or a percentage of every claim (“Copayment”) yourself, you can often decrease your annual premium, but this does not typically waive the waiting period.

- Summary: Different Health Policies and Waiting Periods

Policy Type | Typical PED Waiting Period | Are Riders Available? |

Standard/Comprehensive (e.g., Star Health Assure, HDFC ERGO Optima Secure) | 2 – 3 Years | ✅ Yes, Very Common. Reducers & Consumables riders are often optional. |

Senior Citizen Plans | 1 – 2 Years (often with Mandatory Copay) | ✅ Yes, But Expensive. Specific PED waivers might be available. |

Diabetes/HTN Specific Plans | 30 Days – 1 Year (Highly Targeted) | ❌ No. The plan is the PED cover. |

Group (Employer) Policy | 0 Days (Day 1 Cover) | ❌ No. These terms are non-negotiable by the employee. |

Takeaway: – Never buy a health policy based on price alone. Always check the specific lists of Waiting Periods and Permanent Exclusions in the fine print. Paying an extra 10–15% for a “Consumables” rider or a “PED Reducer” could save you lakhs when you truly need it.

- Reach out to us thru

- Website:-https://herculesadvisors.in/

- Twitter:-https://x.com/NIKHILLJHA

- https://x.com/AdityaD_Shah

- Instagram:-https://www.instagram.com/herculesadvisors/

- Youtube:-https://www.youtube.com/@HerculesInsurance

- Email us on:-nikhiljha159@gmail.com