One of the most stressful experiences is receiving a notification that your claim has been rejected.

This blog simplifies what claim rejection means, the different types you might encounter, and why it happens so frequently in India.

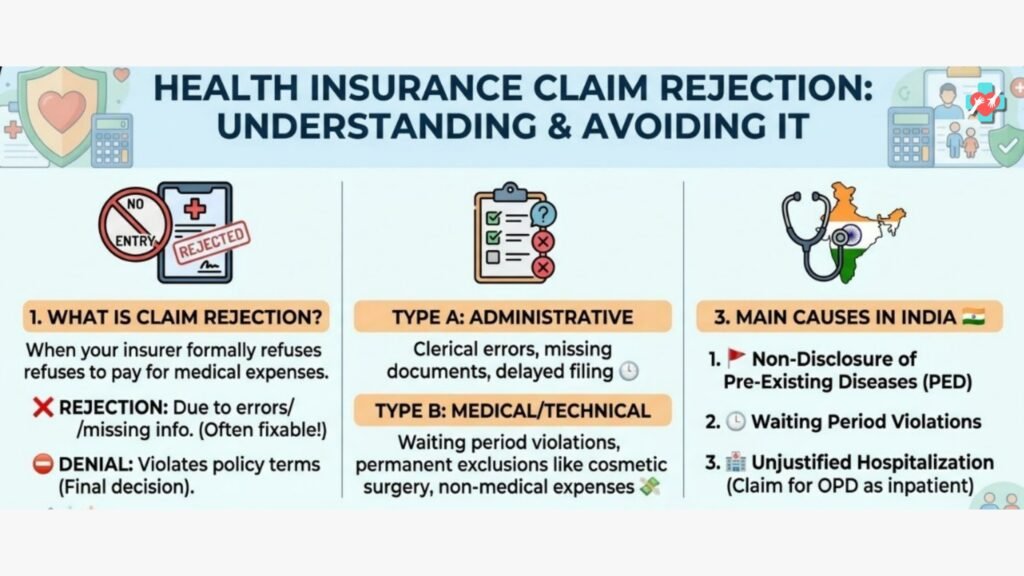

- What is Claim Rejection in Health Insurance?

In simple terms, claim rejection is when an insurance company refuses to pay for the medical expenses you have submitted.

Technically, there is a difference between a Rejection and a Repudiation:

- Rejection:Usually happens at the start of the process due to “clerical” or “procedural” errors (like a missing signature or wrong policy number). You can often fix these and resubmit.

- Repudiation/Denial:This is a more serious, final decision where the insurer denies payment after a full review because the claim violates the policy terms (e.g., claiming for a procedure the policy doesn’t cover).

- Types and Reasons for Rejection

Insurance companies categorize rejections based on where the error occurred. Understanding these can help you avoid them.

Type A: Administrative & Procedural

These occur because the “rules of filing” weren’t followed.

- Delayed Filing:Most insurers require you to intimate them within 24–48 hours of hospitalization. Filing after the deadline is a top reason for rejection.

- Incomplete Documentation:Missing the original discharge summary, hospital bills, or pharmacy receipts.

- Policy Lapse:If you forgot to pay your premium and the “grace period” has passed, the policy is inactive, and no claims will be honored.

Type B: Medical & Technical

These relate to the nature of the treatment itself.

- Waiting Periods:Most policies have a 30-day initial waiting period and a 2–4 year waiting period for specific or pre-existing diseases.

- Permanent Exclusions:Claims for things like cosmetic surgery, obesity treatment, or injuries due to adventure sports are usually excluded from standard plans.

- Non-Medical Expenses:Charges for “consumables” (gloves, masks, nebulizer kits) are often rejected unless you have a specific “OPD” or “Consumables” rider.

- Main Causes for Claim Rejection in India

The Indian insurance market has seen a surge in health policies, but rejection rates remain a concern. According to recent 2024-2025 data, here are the primary culprits:

Cause | Why it happens in India |

Non-Disclosure of PED | The #1 reason. Many applicants hide history of Diabetes or BP to get lower premiums. Under new IRDAI rules, if you hide it, the insurer can reject your claim for up to 5 years (the Moratorium Period). |

Waiting Period Violations | Approximately 25% of rejections happen because policyholders try to claim for surgeries (like Cataract or Kidney stones) before the 2-year mandatory waiting period ends. |

Unjustified Hospitalization | Insurers often reject claims if they feel the patient could have been treated as an “Outpatient” (OPD) and didn’t actually need a 24-hour hospital stay. |

Inaccurate “Proposal Form” | Many Indians let agents fill their forms. If the agent makes a mistake in your age or medical history, the insurer views it as “misrepresentation” and rejects the claim. |

Pro-Tip for 2026

Under the latest IRDAI (Insurance Regulatory and Development Authority of India) guidelines, the “Moratorium Period” has been reduced to 5 years. This means after 5 years of continuous coverage, an insurer cannot reject your claim for non-disclosure unless they can prove a massive, intentional fraud.

- Reach out to us thru

- Website:-https://herculesadvisors.in/

- Twitter:-https://x.com/NIKHILLJHA

- https://x.com/AdityaD_Shah

- Instagram:-https://www.instagram.com/herculesadvisors/

- Youtube:-https://www.youtube.com/@HerculesInsurance

- Email us on:-nikhiljha159@gmail.com