When you think of health insurance, you likely picture the hospital bed, the surgery, and the room rent. But the truth is, your “medical journey” starts long before you check in and continues long after you’re discharged.

In the world of insurance, these are called Pre- and Post-Hospitalization expenses. If you aren’t claiming them, you’re leaving a significant amount of money on the table.

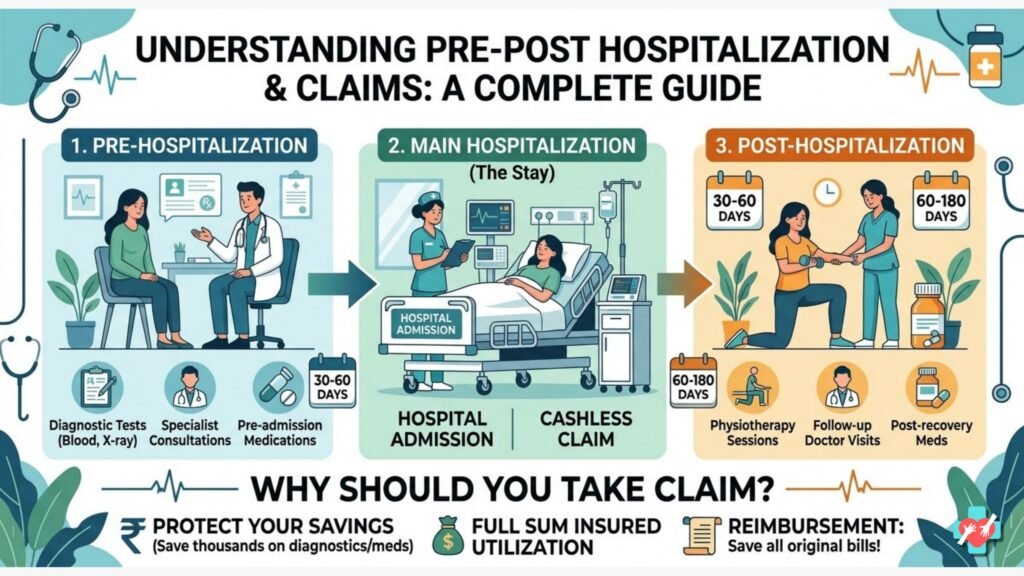

🏥 What is Pre & Post Hospitalization?

Most health insurance policies are designed to be “end-to-end.” They don’t just cover the time you spend inside the hospital; they cover the diagnostic tests that led to the admission and the recovery care that follows.

- Pre-Hospitalization (The “Before” Phase)

This covers medical expenses incurred before you are actually admitted to the hospital.

- What it covers:Specialist consultation fees, blood tests, X-rays, MRIs, CT scans, and medications prescribed to treat the condition that eventually leads to hospitalization.

- The Catch:These expenses are only covered if they are directly related to the illness for which you were hospitalized.

- Post-Hospitalization (The “After” Phase)

This covers expenses incurred after you are discharged to ensure a full recovery.

- What it covers:Follow-up doctor visits, further diagnostic tests to monitor progress, physiotherapy, and long-term medications.

- The Catch:Like pre-hospitalization, these must be for the same ailment you were treated for in the hospital.

⏳ For How Many Days are You Covered?

The duration of coverage depends entirely on your specific policy, but the industry standards generally fall into these brackets:

| Stage | Standard Duration | Premium/Modern Plans |

| Pre-Hospitalization | 30 Days | 60 to 90 Days |

| Post-Hospitalization | 60 Days | 90 to 180 Days |

Pro Tip: Always check your policy document. Some high-end plans now offer up to 180 days of post-hospitalization cover, which is a lifesaver for chronic conditions or major surgeries.

💰 Why Should You Definitely Claim These?

Many people only focus on the “Cashless” part of their hospital stay and forget about the bills they paid out-of-pocket before and after. Here’s why you shouldn’t ignore them:

- High Diagnostic Costs:An MRI or a series of specialized blood tests can cost anywhere from ₹5,000 to ₹15,000. These add up quickly.

- Long-Term Recovery:For surgeries like knee replacements or cardiac procedures, the cost of physiotherapy and follow-up meds over 3-6 months can sometimes equal the cost of the surgery itself.

- Preserves Your Savings:Why dip into your emergency fund for a ₹2,000 consultation or a ₹3,000 lab bill when you’ve already paid a premium for the insurance to cover it?

- Comprehensive Protection:You are entitled to this money. It is part of your “Sum Insured.”

📝 How to File a Successful Claim

Unlike the hospital stay (which is often cashless), pre- and post-hospitalization expenses are usually settled on a reimbursement basis.

- Step 1: Save Every Scrap of Paper.Keep every original bill, pharmacy receipt, and doctor’s prescription.

- Step 2: Link the Treatment.Ensure the doctor’s prescription clearly mentions the diagnosis so the insurer can see it’s the same condition as the hospitalization.

- Step 3: Mind the Deadline.Most insurers require you to submit post-hospitalization claims within 7 to 15 days after the completion of the covered period (e.g., 60 days after discharge).

- Step 4: Submit the Bundle.Submit the claim form along with the discharge summary of your main hospital stay to provide context.

Reach out to us thru

Website:-https://herculesadvisors.in/

Twitter:-https://x.com/NIKHILLJHA

Instagram:-https://www.instagram.com/herculesadvisors/

Youtube:-https://www.youtube.com/@HerculesInsurance

Email us on:-nikhiljha159@gmail.com