Imagine you’re on a long road trip and your fuel tank hits empty. Suddenly, a backup tank kicks in and refills your main tank to the top—for free.

In health insurance, that’s exactly what a Restoration Benefit does. It’s a safety net that recharges your insurance coverage if you use it all up during the year.

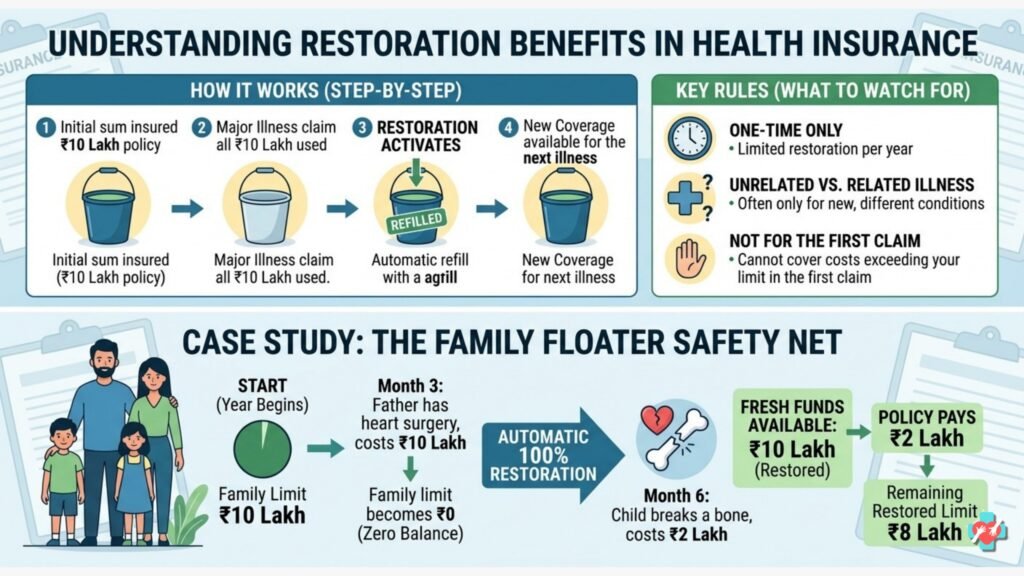

How Does It Actually Work?

When you buy health insurance, you choose a “Sum Insured” (e.g., ₹5 Lakh). Usually, once you claim ₹5 Lakh, your coverage for that year is over. But with a Restoration Benefit, the company resets your balance back to ₹5 Lakh.

There are two main ways this “reset” happens:

- Complete Exhaustion:The refill only triggers when your balance hits zero.

- Partial Exhaustion:The refill triggers after any If you have a ₹5 Lakh cover and use ₹2 Lakh, the company immediately puts that ₹2 Lakh back so you’re at ₹5 Lakh again.

Nowadays, Insurance companies has introduced “Unlimited Restoration” with an advance benefit to get now refill for multiple times in a same year up to Sum insured.

Why is this Useful?

To see the true value, let’s look at a Family Floater Plan (where one policy covers the whole family).

The Scenario:

- Family:Rahul, his wife Priya, and their son.

- Policy Limit:₹5 Lakh with 100% Restoration.

Month 3: Rahul has a major surgery that costs ₹5 Lakh. The policy pays the bill, but now the family’s coverage for the rest of the year is ₹0.

The “Restoration” Magic:

Without restoration, if Priya fell ill a month later, Rahul would have to pay from his pocket. But because they have the Restoration Benefit, the insurance company automatically refills the “bucket.” Priya now has a fresh ₹5 Lakh available for her treatment.

Key Takeaway: It prevents one family member’s major illness from leaving the rest of the family unprotected.

3 “Hidden” Rules You Must Know

Salespeople often forget to mention these details, but they are crucial:

- Different Illness vs. Same Illness:Some policies only refill if the second illness is different from the first. If you go back to the hospital for the same heart issue, the refill might not kick in. Look for plans that allow “Same Illness” restoration.

- The “First Claim” Rule:Restoration cannot be used to pay for your very first bill of the year if it exceeds your limit. If your bill is ₹7 Lakh and your limit is ₹5 Lakh, you must pay the extra ₹2 Lakh yourself. The refill only helps with the next time you go to the hospital.

- Use It or Lose It:The restored amount does not carry forward to next year. If you don’t use the “refilled” money by the end of the policy year, it disappears.

Conclusion: Is it worth it?

In today’s world, where medical costs are rising, a Restoration Benefit is like having a “spare tire” for your finances. It’s especially essential for:

- Families(where multiple people share one limit).

- Senior Citizens(who might need to visit the hospital more than once).

- People with lower sum insured(who want extra protection without paying for a massive base policy).

Next time you renew your policy, ask: “Does my plan have partial restoration, and does it cover the same illness?”

Reach out to us thru

Website:-https://herculesadvisors.in/

Twitter:-https://x.com/NIKHILLJHA

Instagram:-https://www.instagram.com/herculesadvisors/

Youtube:-https://www.youtube.com/@HerculesInsurance

Email us on:-nikhiljha159@gmail.com