In the Indian health insurance market, many policyholders are surprised when their claims are only partially paid, even if they have a high sum insured. Often, the culprit is a small but powerful clause: Reasonable and Customary (R&C) Charges.

As an educator in health insurance, I want to help you decode this “hidden” term so you aren’t left with an unexpected hospital bill.

- What are Reasonable and Customary Charges?

In India, hospital charges are not strictly regulated by the government. A hospital in South Mumbai might charge ₹1.5 Lakh for a procedure, while a similar-grade hospital in a smaller suburb might charge ₹80,000 for the exact same surgery.

Reasonable and Customary Charges refer to the amount that an insurer considers “fair” for a specific treatment based on:

- Geographical Location: Rates are compared within the same city or zone.

- Hospital Grade: A premium multi-specialty hospital is compared against other hospitals of similar infrastructure.

- Standard Prevailing Rates: The average cost charged by most providers in that area for that specific diagnosis.

The Logic: If your hospital charges significantly more than the “customary” rate for your city, the insurer will pay the average rate and ask you to pay the difference.

- Key Clauses to Watch For

Under IRDAI (Insurance Regulatory and Development Authority of India) guidelines, this clause is standard, but its application can vary. Look for these specific mentions in your policy:

- The “Medically Necessary” Link: R&C charges usually apply only to treatments deemed “Medically Necessary.” If a doctor orders extra tests that aren’t standard for your condition, the insurer may classify them as “unreasonable.”

- Associate Medical Expenses: This is where R&C hits hardest. It includes Surgeon fees, Anaesthetist fees, and Operation Theatre (OT) charges. Even if you have “No Room Rent Capping,” these associate fees are often still capped by what is “Reasonable and Customary.”

- PPN (Preferred Provider Network) Rates: Many Indian insurers (like those in the GIPSA network) have pre-negotiated “Package Rates” with specific hospitals. If you go outside this network, the R&C clause is almost always invoked to match these package rates.

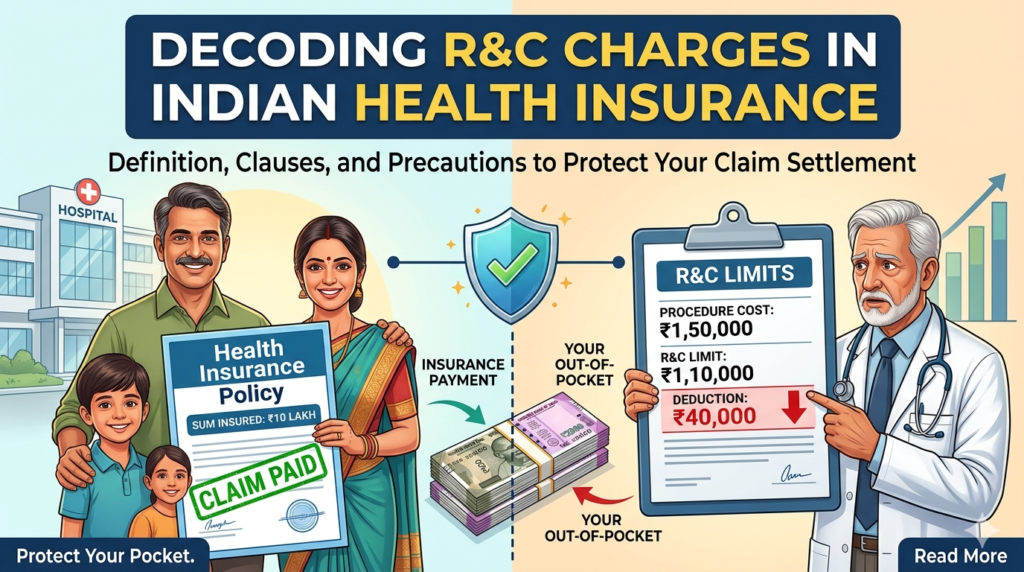

- The “Financial Trap”: An Example

Imagine you have a ₹10 Lakh policy. You undergo a gallbladder surgery.

- Hospital Bill: ₹1,50,000

- Insurer’s R&C Limit for your city: ₹1,10,000

- Result: The insurer pays ₹1.1 Lakh. You pay ₹40,000 out of pocket, despite having a ₹10 Lakh cover.

- Precautions: How to Protect Yourself

To ensure your claim is settled fully, follow these steps before and during hospitalization:

- Prioritize Network Hospitals

Hospitals in your insurer’s Network or PPN have already agreed to specific “Tariff Cards.” In these cases, the “Reasonable and Customary” dispute rarely happens because the price is pre-fixed.

- Get a Written Estimate

For planned surgeries, ask the hospital for a detailed “Cost Estimate.” Send this to your insurer or TPA (Third Party Administrator) for Pre-Authorization. If they approve the amount in writing beforehand, they cannot easily invoke the R&C clause later.

- Compare “Like-for-Like”

If you choose a high-end hospital, check if their rates for your specific surgery are more than 15-20% higher than other similar hospitals in the same area. If they are, be prepared for a partial deduction.

- Avoid “Package Padding”

Ask the hospital billing department if they are adding unnecessary “service charges” or “administrative fees.” Insurers almost always strike these out under the R&C clause.

What if your claim is already reduced?

If your claim was short-settled citing “Reasonable and Customary,” you have the right to ask the insurer for the data/benchmark they used to reach that conclusion. If they cannot justify it with local rate comparisons, you can escalate the matter to the Insurance Ombudsman.