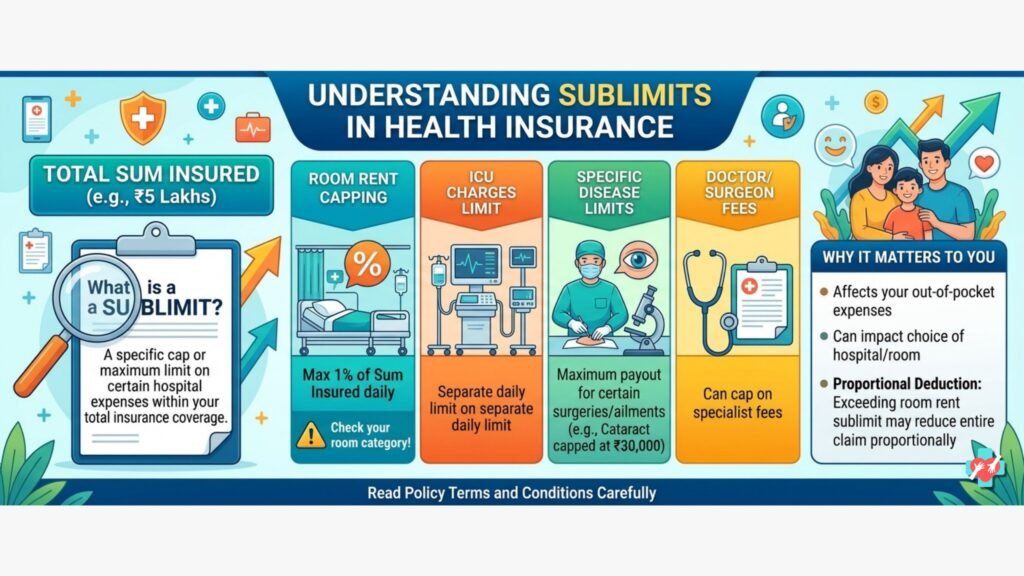

Sub-limit: – Do you know your Health Insurance policy has limitation?

Sub-limit is a clause in a health insurance policy that the insured person has to pay a fixed amount to specific illness, condition, diagnostic tests or procedures at time of claim. Mostly the insurer has fixed a maximum claim amount for certain planned treatments. Common examples include cataracts, kidney stones, hernia, or tonsillectomy.

For instance, if your policy has a ₹30,000 sub-limit for cataract surgery and the hospital bill comes to ₹50,000, the insurance company will only pay ₹30,000. You would have to pay the remaining ₹20,000 out of your own pocket.

Feature | Positives | Negatives |

Premium Cost | Policies with sub-limits usually have lower premiums, making them more affordable. | You save money upfront but may face high out-of-pocket costs during a claim. |

Financial Planning | Good for people on a very tight budget who want basic “safety net” coverage. | Can lead to financial stress if the actual hospital bill far exceeds the limit. |

Treatment Choice | None. | Often forces you to choose cheaper hospitals or general wards to stay within the limit. |

Claim Process | None. | Can lead to disputes and disappointment when the full claim isn’t reimbursed. |

Why You Should Avoid Policies with Sub-limits

Most experts recommend choosing a policy without sub-limits (or with minimal ones) for the following reasons:

- Medical Inflation:The cost of surgery today might be ₹50,000, but in five years, it could be ₹80,000. If your sub-limit is fixed at ₹40,000, your “protection” weakens every year.

- Unpredictable Complications:A standard procedure can become expensive if complications arise. Sub-limits usually don’t account for extra days in the ICU or additional medications.

- Hidden Costs:Sub-limits on Room Rent are particularly dangerous. If you exceed your room rent limit, many insurers apply “proportional deduction,” where they reduce your entire claim amount (doctors’ fees, surgery costs, etc.) proportionately.

- Peace of Mind:The primary goal of insurance is to remove the burden of hospital bills. A sub-limit brings that burden back to you at the worst possible time.

Summary Checklist

When buying a policy, always check the “Policy Wordings” for:

- Disease-wise sub-limits:Caps on specific surgeries.

- Room Rent limits:Caps on the daily hospital room charges (look for “No Room Rent Capping”).

- Co-payment:A clause where you agree to pay a percentage of every claim (this is different from a sub-limit but also increases your costs).

- Reach out to us thru

- Website:-https://herculesadvisors.in/

- Twitter:-https://x.com/NIKHILLJHA

- https://x.com/AdityaD_Shah

- Instagram:-https://www.instagram.com/herculesadvisors/

- Youtube:-https://www.youtube.com/@HerculesInsurance

- Email us on:-nikhiljha159@gmail.com